What is Alumis's Envudeucitinib valuation?

Alumis's shares soared after Envudeucitinib was successful in a Phase 3 trial in psoriasis but it enters a competitive market. Will the drug be a success for Alumis?

FEBRUARY 2ND 2026

When it comes to treatment options for plaque psoriasis the start of 2026 has been very similar to 2025. Alumis recently reported positive results from their Phase 3 trials ONWARD1 and ONWARD2 which tested Envudeucitinib against a placebo and Apremilast in moderate to severe plaque psoriasis.

This news comes on the heels of Takeda’s own TYK2 inhibitor Zasocitinib reporting positive results from their Phase 3 trial in December 2025 and J&J also reporting positive results from their IL-23 receptor blocker Icotrokinra in July 2025.

All three companies are now racing to get their oral drug approved for this indication and primed to enter a 40 billion dollar psoriasis market that has long been dominated by biologic injections.

So at The Pipeline we wanted to answer an important question, what is Envudeucitinib’s valuation?

Results of ONWARD 1&2 Trials

According to the press release and investor presentation, Alumis said 74% of the trial participants who received Envudeucitinib (n=420) achieved a PASI 75 response (75% clearance of skin lesion) after 4 months. Complete skin clearance (PASI 100) was seen in more than 40% of trial participants.

Dr. Jorn Drappa, Alumis’s chief medical officer said in the press release that “Maximally inhibiting TYK2, envudeucitinib blocks both IL‑23 and IL‑17 to deliver comprehensive disease control. In Phase 3, this translated into rapid onset of action, high rates of skin clearance, and meaningful symptom improvements that rank among the strongest reported for an oral therapy.”

Envudeucitinib was reported to be well tolerated, with most adverse events being mild-to-moderate and transient.

How we arrived at our valuation (powered by PharmaCalc)

Our valuations are built on PharmaCalc, and below is our Gantt chart outlining the key events of Envudeucitinib since it announced it’s positive Phase 3 trial results.

Below are some key inputs and variables that we want to explain so we can show we built our valuation.

Our model anticipates that it will take 18 months for Envudeucitinib to be approved and have it at a 94% probability of it being approved based on PharmaCalc benchmarks.

We believe Envudeucitinib will start generating revenue in 2028 with a LOE in 2039.

Icotrokinra already reported topline positive results in July 2025 and we expect an approval by Q1 2027.

Zasoctinib reported out positive topline results in December 2025 and we anticipate their approval in Q3 2027.

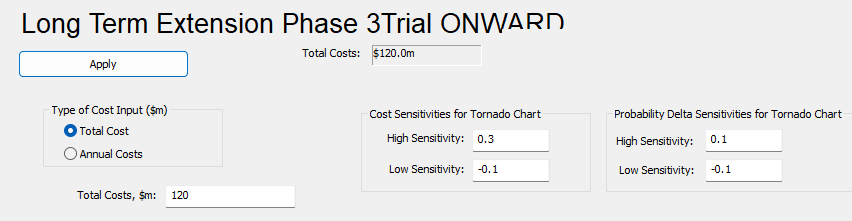

We did not include the already reported positive Phase 3 trials as this is sunk cost for Alumis but we included the cost of running the ongoing Long Term Extension Phase 3 trial ONWARD3 (see below) which is evaluating the long term efficacy of Envudeucitinib and will be completed in 2028. Based on our benchmarks from PharmaCalc we anticipate that this trial will cost $120 million dollars.

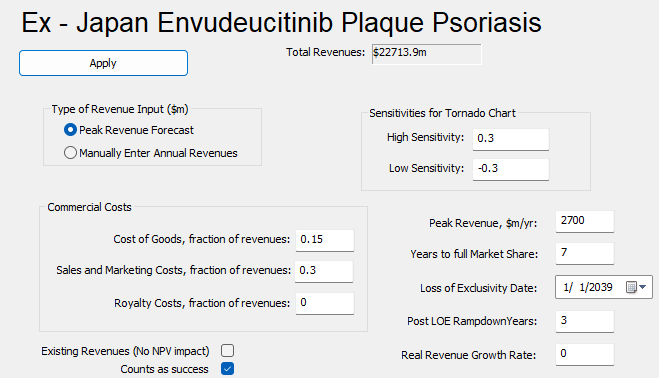

When we were trying to estimate revenues, we used Apremilast as our benchmark. Peak sales for Apremilast was $2.5 billion dollars and we anticipate based on the positive results and best-in-class profile with manageable toxicities, that peak revenues for Envudeucitinib would be $2.7 billion dollars and would take seven years to achieve full market share since this is their first launch. In PharmaCalc we can estimate cost of goods and cost of sales marketing, which was set at 15% and 30% of revenues respectively (see below.)

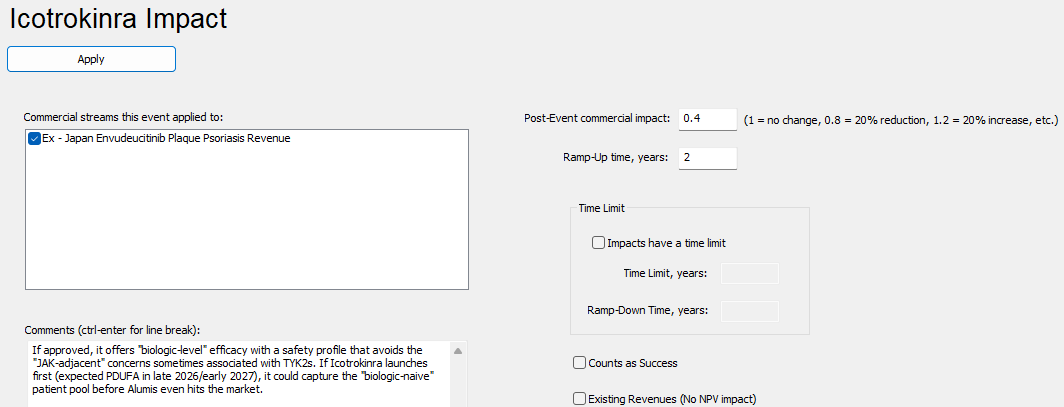

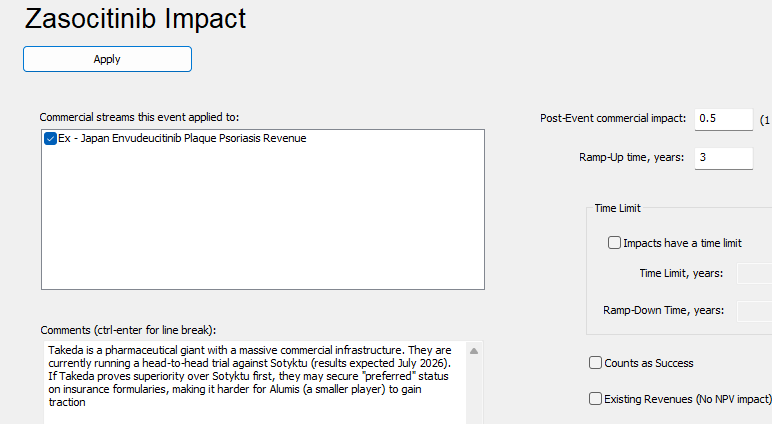

PharmaCalc allows users to add market events (denoted by the gray triangles) onto our Gantt chart which is defined by competitors in the market. In the case of Alumis, both J&J and Takeda represent significant competition as both are all targeting the same patient population and are oral once daily medications. In our estimation both Icotrokinra and Zasocitinib will have a major negative impact on Envudeucitinib’s revenue (see below.)

So what is the valuation of Envudeucitinib

According to our modeling, PharmaCalc calculated the Expected Net Present Value (eNPV) of Envudeucitinib at $622 million dollars. PharmaCalc also produces a Commercial Value Given Success number (CVGS) which gives a dollar value of how much the product is worth when it gets to market, and according to PharmaCalc, we think Envudeucitinib is worth $772 million.

We can also calculate Investment Efficiency (IE), which helps companies understand how good an investment is. According to PharmaCalc, Envudeucitinib’s IE is 6, in other words for every dollar invested by Alumis will return $6 dollars in value, making this an efficient investment.

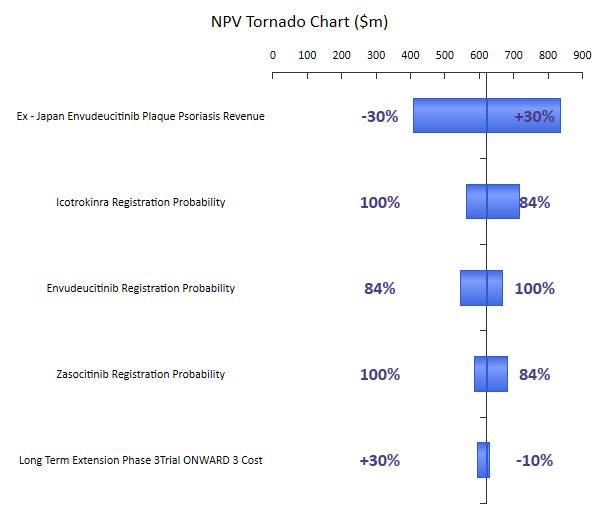

As part of our model and valuation, we ran an NPV Tornado chart to better understand which parameters will have the most impact on it’s eNPV. The highest degree of variability that our model found was the revenue with a 30% swing in either direction generating a revenue range from $400 - 800 million dollars.

Can Envudeucitinib meet it’s potential valuation?

So what does PharmaCalc’s valuation tell us about Envudeucitinib and Alumis. In short, our model agrees with the positive investor sentiment that followed the announcement; with shares more than doubling since the results were announced earlier this month.

From an efficacy standpoint, Envudeucitinib and Icotrokinra produced similar results with both trials showing high PASI 75 and PASI 90 response rates at week 16 and week 24. Both appear to be more effective than the current TYK2 inhibitor from BMS Deucravacitinib; although notably Envudeucitinib was compared to Apremilast whereas Icotrokinra was compared directly against Deucravacitinib.

Alumis has noted that Envudeucitinib is best-in-class with maximal TYK inhibition and a manageable toxicity profile. According to their investor presentation, they believe twice-a-day scheduling is more convenient than their once-a-day competitors because Envudeucitinib has no dietary restrictions. Perhaps, this will be the case, but published literature has consistently shown that once daily pills are always more convenient.

The other major question that faces Alumis, is the relative lack of success of Deucravacitinib (approved in 2022). In 2024 BMS reported sales of $246 million. One major reason for the lack of sales includes safety concerns that are part of all JAK2 medications. BMS was able to avoid a black box warning allowing it promote its safety, but despite the clean label, both dermatologists and patients have been reluctant to use it.

Of course, the cost of Envudeucitinib will play a major role in sales. With rising premiums, and expiring subsidies, there’s an increased scrutiny on drug pricing as a major driver of healthcare costs. More pharmaceutical companies are moving towards a direct to consumer strategy, including BMS who started offering Deucravacitinib directly to consumers at a heavily discounted price to boost sales. Alumis should consider this as well to provide more accessible prices for patients especially as it tries to compete with Takeda and J&J who are bigger companies, with deeper pockets.

Caveats aside, there remains a major need for better oral therapeutics in moderate-to-severe plaque psoriasis and if successful (like our model thinks it will be) Envudeucitinib can end up having a major positive impact on these group of patients.